Loan Against Property Calculator: EMI, Eligibility and Interest Rate Guide 2026

Quick Answer

A Loan Against Property (LAP) lets you borrow 50–70% of your property's market value at interest rates of 8.5–15% p.a. Monthly EMI is calculated using: EMI = P × r × (1+r)^n ÷ [(1+r)^n − 1]. Use our free LAP EMI calculator to instantly find your monthly payment, total interest, and check eligibility

Key Takeaways

- ✓ You can borrow 50–70% of your property's current market value through a Loan Against Property

- ✓ LAP interest rates range from 8.5% to 15% p.a. - lower than personal loans, higher than home loans

- ✓ Loan tenure can go up to 15–20 years, which keeps your monthly EMI affordable

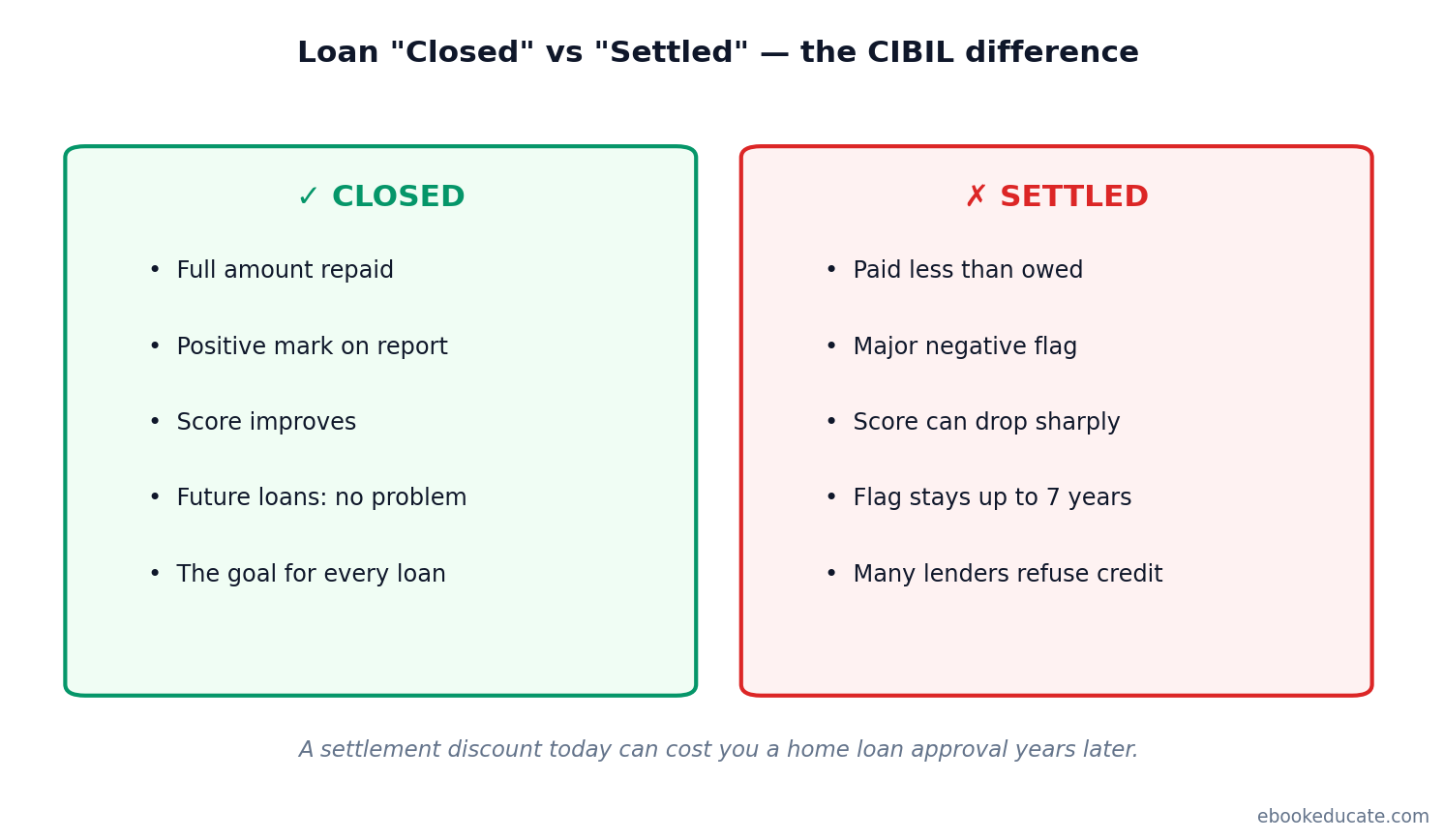

- ✓ A CIBIL score of 750+ gets you the best rates; minimum required is usually 650

- ✓ LAP funds can be used for any purpose - business, education, medical, or debt consolidation

If you own a property in India and need funds for business, education, medical emergencies, or debt consolidation - a Loan Against Property (LAP) can be one of the smartest borrowing options available to you.

Use the EbookEducate Loan Against Property Calculator to instantly calculate your monthly EMI, total interest payable, and get a full amortization breakdown — before you even walk into a bank.

What is a Loan Against Property?

A Loan Against Property is a secured loan where you pledge your residential or commercial property as collateral to borrow money from a bank or NBFC. Unlike a home loan (which is used only to buy a house), a LAP can be used for any purpose.

You keep ownership and use of your property throughout the loan tenure. The bank only has a charge on it until the loan is fully repaid.

Key facts: - Loan amount: 50–70% of property's market value - Tenure: Up to 15–20 years - Interest rate: 8.5–15% p.a. - Purpose: Business, education, medical, travel, debt consolidation — anything

How to Use the EbookEducate LAP EMI Calculator

The calculator needs just 3 inputs:

| Input | Example |

|---|---|

| Property Value (₹) | ₹80,00,000 |

| Loan Amount (₹) | ₹50,00,000 (keep within 60–70% of property value) |

| Interest Rate (% p.a.) | 10.5% |

| Loan Tenure (years) | 15 |

Instant output you get: - Monthly EMI - Total interest payable - Total amount paid - Full month-by-month amortization table

LAP EMI Calculation Formula

The formula used to calculate LAP EMI is the same as any term loan:

EMI = P × r × (1+r)^n ÷ [(1+r)^n − 1]

Where: - P = Principal loan amount - r = Monthly interest rate = Annual Rate ÷ 12 ÷ 100 - n = Loan tenure in months

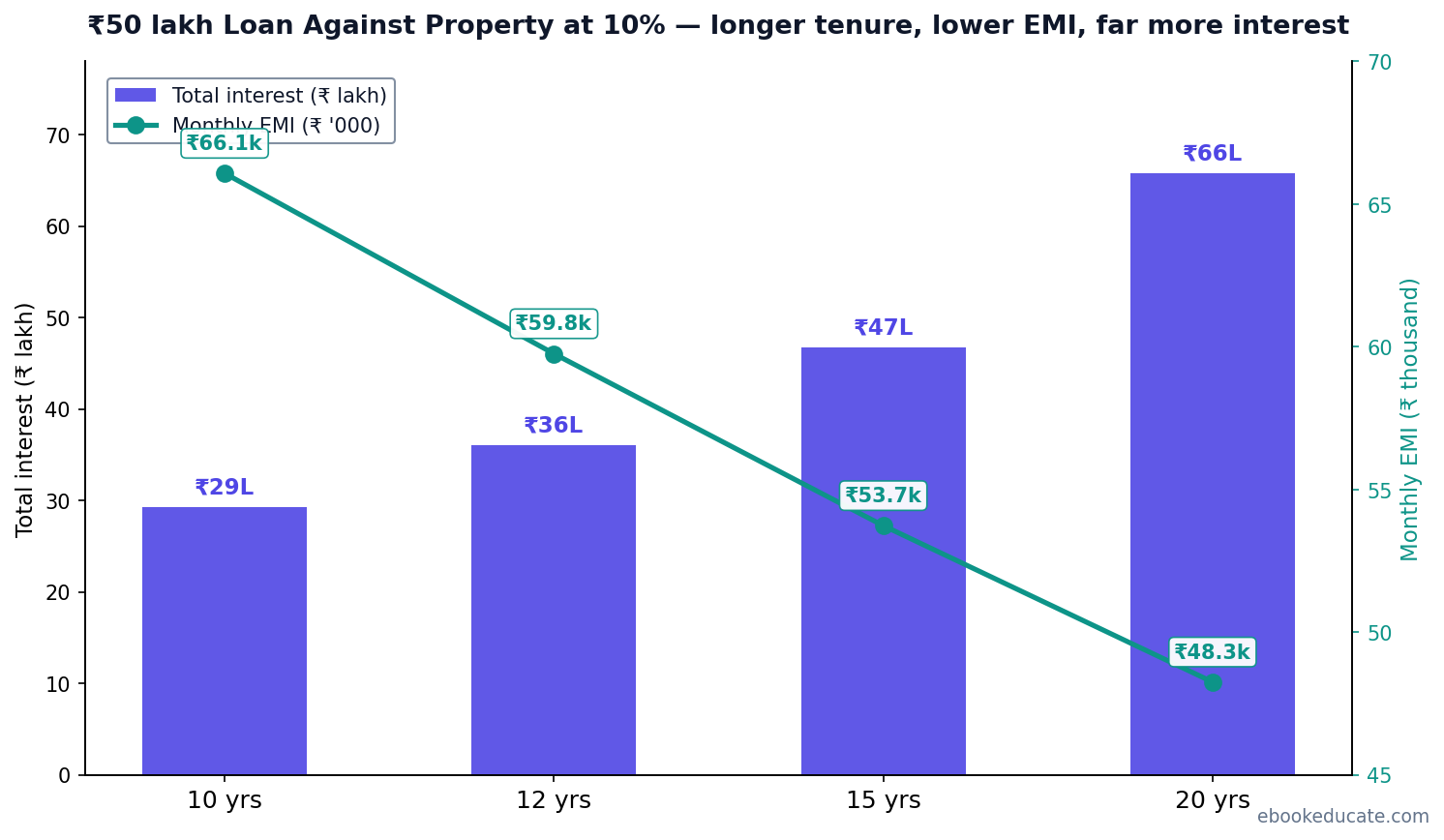

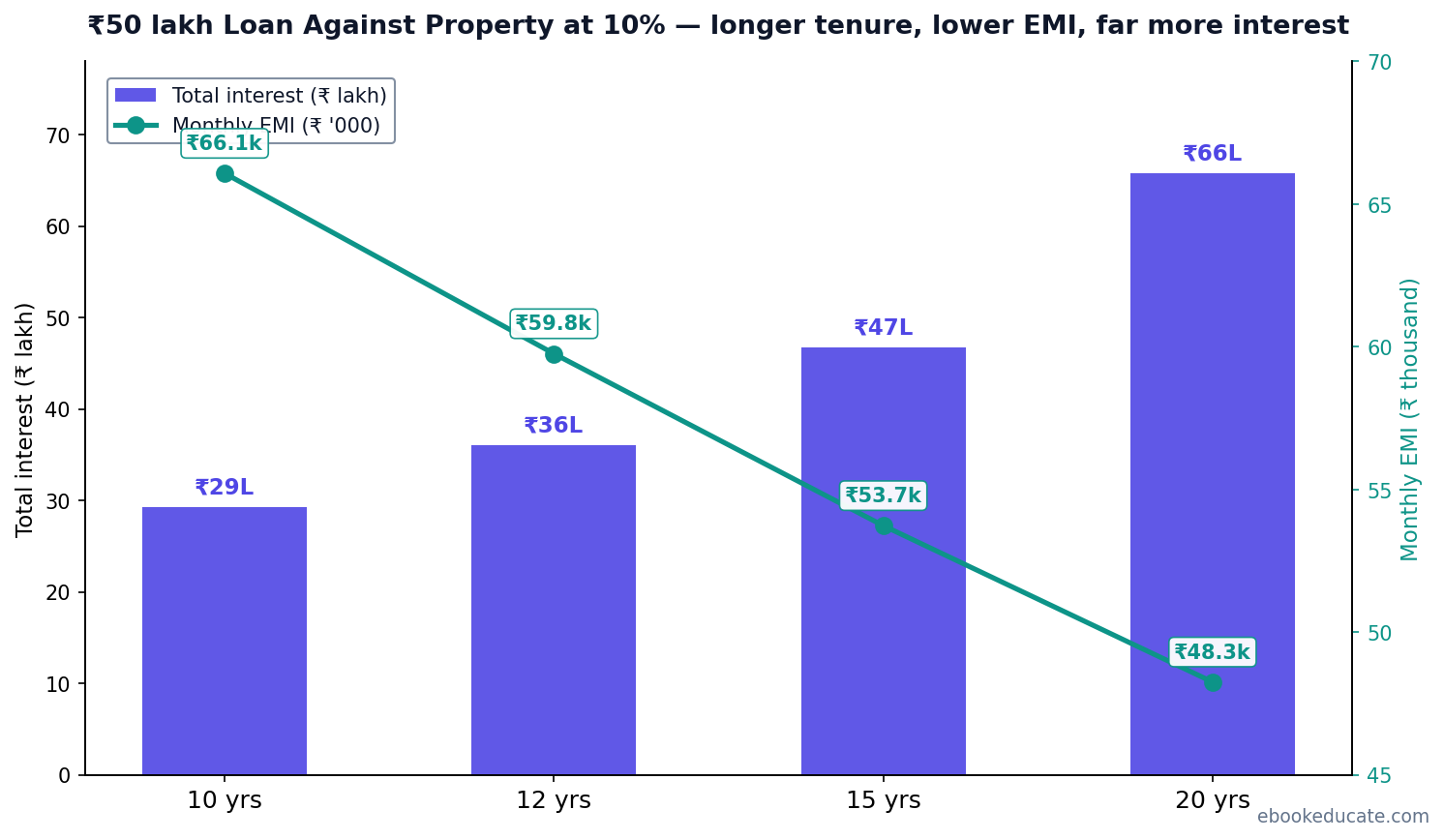

Example Calculation

Loan amount: ₹50 lakhs | Interest rate: 10% p.a. | Tenure: 15 years

Loan amount: ₹50 lakhs | Interest rate: 10% p.a. | Tenure: 15 years

- r = 10 ÷ 12 ÷ 100 = 0.00833

- n = 15 × 12 = 180 months

- EMI = ₹53,730 per month

- Total interest paid = ₹46,71,400

- Total amount paid = ₹96,71,400

A 15-year tenure keeps EMI manageable, but you pay nearly as much in interest as the principal. Use our calculator to compare tenures.

Current Loan Against Property Interest Rates (2025)

| Lender | Interest Rate (p.a.) | Processing Fee |

|---|---|---|

| SBI | 9.15% – 10.50% | 1% of loan amount |

| HDFC Bank | 9.50% – 11.00% | Up to 1.5% |

| ICICI Bank | 9.75% – 12.00% | Up to 2% |

| Axis Bank | 9.90% – 12.50% | 1% |

| Bajaj Finance | 9.75% – 13.00% | Up to 2% |

| PNB Housing Finance | 9.50% – 12.75% | 0.5–1% |

Note: Rates are indicative and subject to change. Final rate depends on your CIBIL score, income, loan amount, and property valuation.

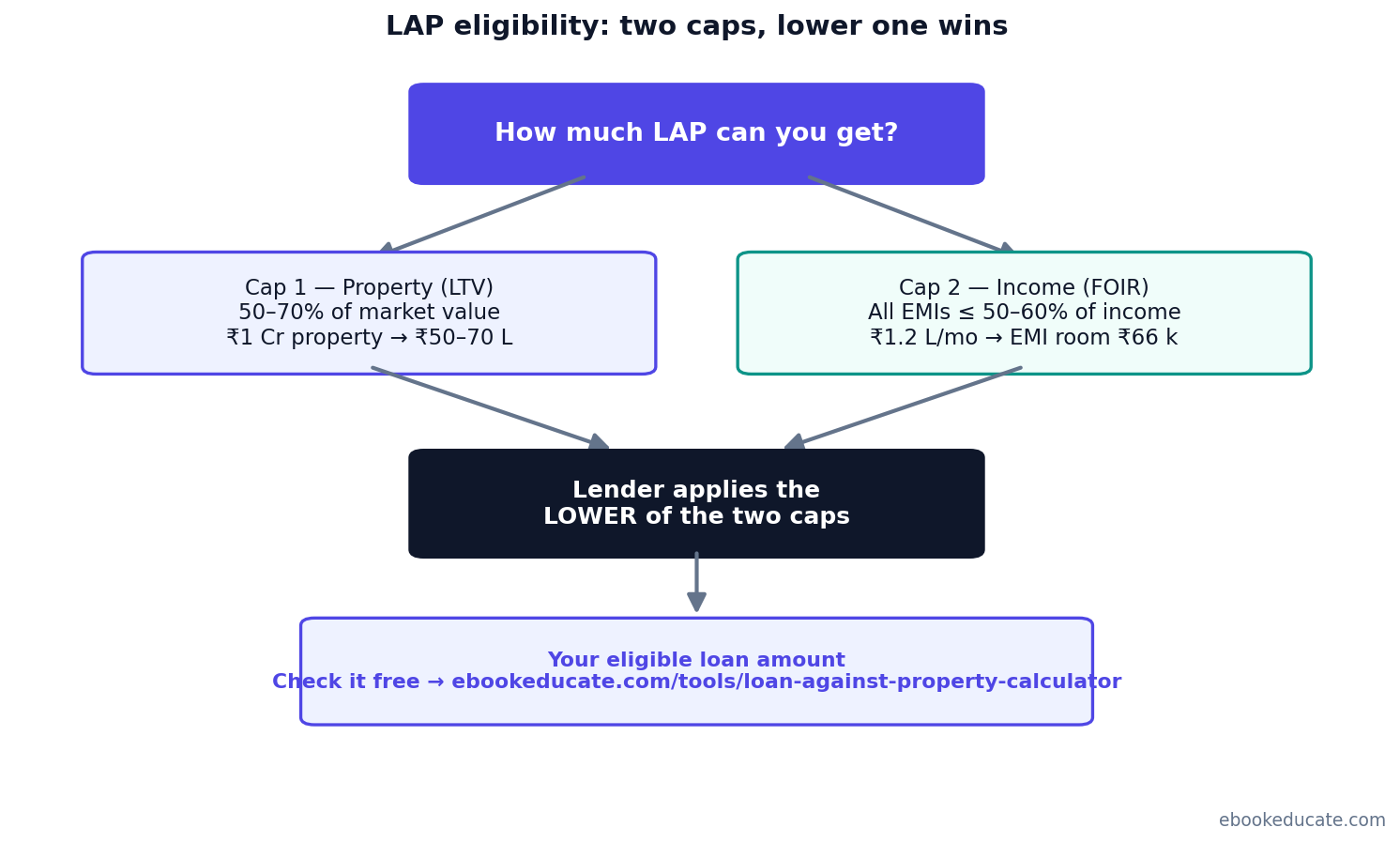

Loan Against Property Eligibility Criteria

For Salaried Individuals:

- Age: 21–60 years

- Employment: Minimum 2–3 years with current employer

- Net monthly income: Usually ₹25,000+

- CIBIL score: 700+ preferred (650 minimum at most lenders)

- EMI obligation: Existing EMIs + new LAP EMI should not exceed 50–60% of monthly income

For Self-Employed Individuals:

- Age: 21–65 years

- Business vintage: Minimum 3 years of profitable operations

- ITR: 2–3 years of filed returns

- CIBIL score: 700+ preferred

Property Criteria:

- Clear and marketable title

- No existing mortgage or encumbrance

- Approved by local municipal authority

- Valuation done by bank-empanelled valuer

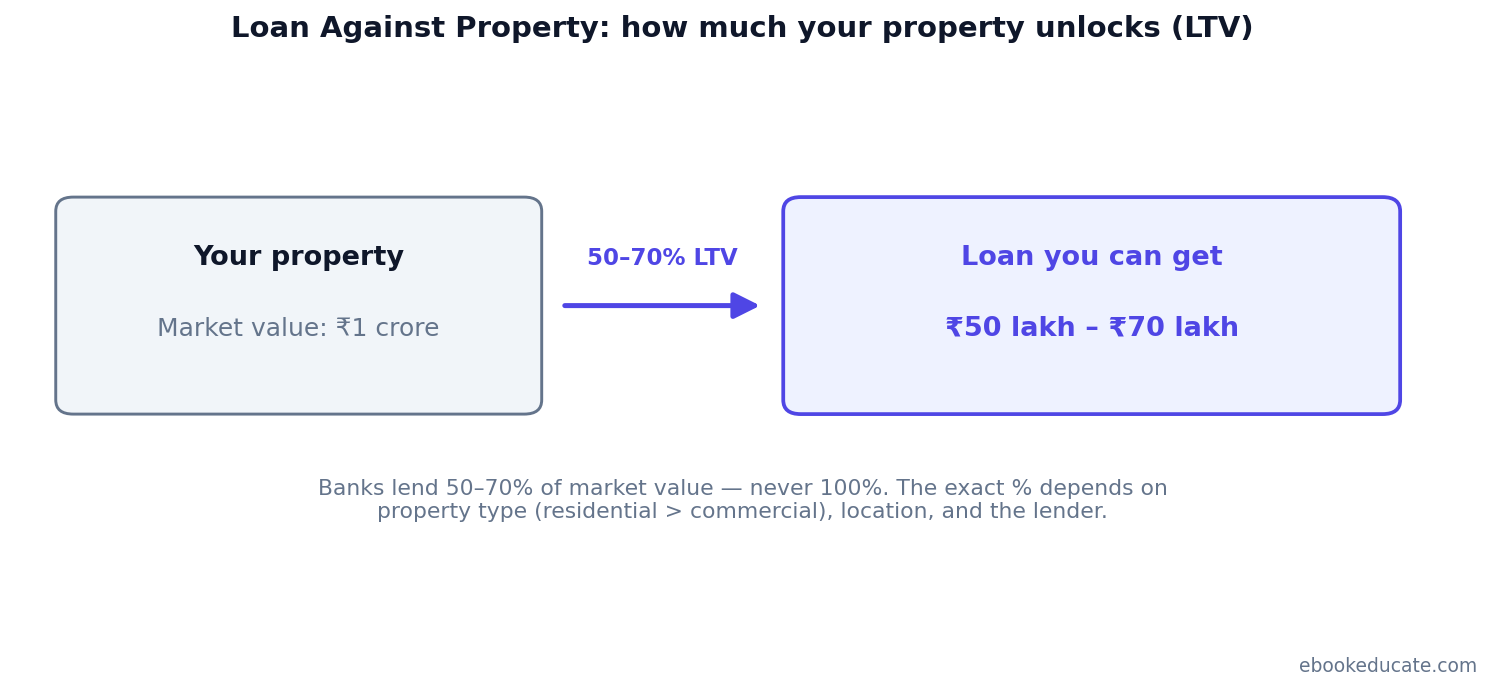

Loan-to-Value (LTV) Ratio — What It Means for You

LTV determines how much of your property's value you can borrow:

| Property Value | Max LTV | Max Loan Amount |

|---|---|---|

| ₹30 lakhs | 60% | ₹18 lakhs |

| ₹50 lakhs | 65% | ₹32.5 lakhs |

| ₹1 crore | 70% | ₹70 lakhs |

| ₹2 crore | 65% | ₹1.3 crores |

Higher-value properties in metro cities typically get better LTV ratios. Rural or semi-urban properties may get only 50–55%.

LAP vs Home Loan vs Personal Loan

| Feature | LAP | Home Loan | Personal Loan |

|---|---|---|---|

| Interest Rate | 8.5–15% | 8–9.5% | 10–24% |

| Loan Amount | Up to ₹10 Cr | Up to ₹15 Cr | Up to ₹40 lakhs |

| Tenure | Up to 20 years | Up to 30 years | Up to 7 years |

| Collateral | Required | Required | Not required |

| End-use restriction | None | Only property purchase | None |

| Tax benefit | No | Yes (80C + 24b) | No |

| Processing time | 7–15 days | 7–20 days | 1–5 days |

LAP is best when: You need a large amount at a lower interest rate and have property to offer as security.

Documents Required for Loan Against Property

KYC Documents:

- Aadhaar card

- PAN card

- Passport / Voter ID (address proof)

- 2 recent passport photographs

Income Documents:

Salaried: Last 3 months' salary slips, Form 16, last 6 months' bank statements Self-employed: Last 2–3 years' ITR with computation, CA-certified P&L and balance sheet, last 12 months' bank statements

Property Documents:

- Original sale deed / title deed

- Property tax receipts (last 3 years)

- Society NOC / encumbrance certificate

- Approved building plan / layout

- Municipal corporation receipt

How to Improve Your LAP Eligibility

- Improve your CIBIL score - Pay all existing EMIs and credit card bills on time. Aim for 750+.

- Reduce existing debt - Close small loans before applying. Lower your Fixed Obligation to Income Ratio (FOIR).

- Add a co-applicant - Spouse or working child can increase the eligible loan amount.

- Choose a longer tenure - This reduces EMI burden and improves FOIR.

- Get the property valued properly - Use an experienced, bank-approved valuer to maximise the assessed value.

Conclusion

A Loan Against Property is one of the most cost-effective ways to access large funds in India - especially compared to personal loans or credit card debt. With interest rates starting at 8.5% and tenures up to 20 years, it's a powerful tool when used wisely.

Before approaching any bank, use the EbookEducate LAP Calculator to know exactly what EMI to expect, how much you'll pay in total interest, and which tenure works best for your budget.

Also check: Home Loan Eligibility Calculator | Personal Loan EMI Calculator | EMI Calculator